Howard Lau, Investor, Coach, Speaker

Menu

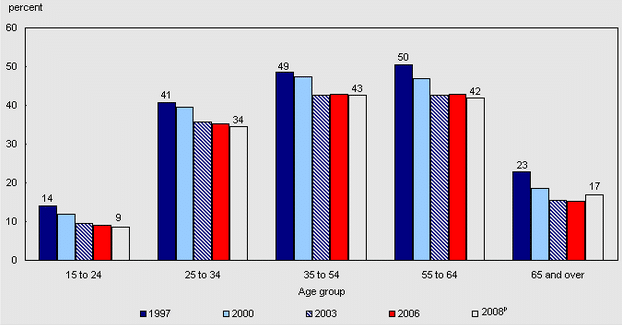

Secure Your Tomorrow: A Guide to Registered Retirement Saving Plans (RRSPs)

Nowadays, a person needs security for their financial future in an environment where everything is moving so fast that a person’s eyes cannot follow it. Investing in Registered Retirement Savings Plans (RRSPs) will go a long way toward ensuring financial stability in your post-retirement period. This is a complete walk-through on RRPS, why it is essential, its eligibility, and how to maximize it as an investment option.

Understanding RRSPs: An Introduction

The Canadian government has approved accounts known as Registered Retirement Saving Plans (RRSP) that are intended to help motivate Canadians to prepare for retirement. Having different forms of tax advantage, they are preferred by those who desire planning for their tomorrow.

Benefits of RRSPs: Why You Should Consider Them

Tax Deductible Contributions:

Find out how this may help lower your taxable income, thus reducing your burden today.

Tax-Deferred Growth:

Find out how you can benefit from tax-free growth of your money until withdrawal as your investment compounds over time.

Wide Range of Investment Options:

Comprehend the flexibility of investment options that allows you to tailor-make your portfolio according to your risk tolerances and financial objectives.

Wide Range of Investment Options:

Comprehend the flexibility of investment options that allows you to tailor-make your portfolio according to your risk tolerances and financial objectives.

Eligibility and Contribution Limits

Eligibility Criteria:

Learn more about whom they encompass and why it's essential to measure your financial status before paying in.

Contribution Limits:

You have to learn about the annual contribution guidelines established by the government and what happens when it is overstepped, resulting in financial penalties.

Contribution Limits:

You have to learn about the annual contribution guidelines established by the government and what happens when it is overstepped, resulting in financial penalties.

RRSP Investment Options: Making Informed Choices

Mutual Funds and ETFs:

Gain a basic understanding of these widely-used investment choices and their use in enhancing your RRSP holdings.

Stocks and Bonds:

Discuss risk factors involved while investing in individual stocks and bonds in an RRSP.

Planning Your RRSP Investments: Tips and Strategies

Dollar-Cost Averaging:

Understand how this method will protect your investment against the adverse effects of fluctuating markets.

Rebalancing Your Portfolio:

Remember that occasionally, you must readjust your investment to fit in with your changeable risk potential and monetary targets.

Withdrawing from RRSPs: What You Need to Know

Tax Implications:

Tax implications of withdrawing from an RRSP before and after retirement.

Home Buyer's Plan and Lifelong Learning Plan:

These programs enable you to withdraw from your RRSP for specific reasons.

Planning for the Future: Maximizing RRSP Benefits

Spousal RRSPs:

Find out how these accounts can balance out retirement-income differences between spouses, which may be tax deductible.

Estate Planning:

Find out how to name beneficiaries and ensure it's easy to transfer RRSP property when death comes your way.

Conclusion

Finally, RRSPs are potent instruments that make a significant difference in your life financially. Knowing what benefits, who is eligible, and how they invest for tomorrow will help to decide how to save. Begin organizing and have a pleasant retirement tomorrow.

About hay2brick

Discover Hay2Brick:

Your Trusted Canadian Real Estate Investment Partner. We specialize in multi-family properties across the USA, leveraging 15+ years of expertise for strong cash flow and appreciation. Explore secure, profitable opportunities with our seasoned team.

Frequently Asked Questions (FAQs)

Q1: Do I need to pay the additional premium despite having a pension at work?

Can one with an office pension plan save in an RRSP? On the other hand, your pension plan might eat into your contribution room.

Q2: What is the person's age who can contribute to RRSPs?

There is no upper age for participating in RRSPs. Furthermore, if you still generate earnings, you could continue contributing to your RRSP.

Q3: Do I qualify to use my RRSP money for educational purposes?

Yes, you can draw money from your RRSP through the LLP to pay tuition fees towards your study or that of your spouse/common-law partner.

Q4: What would happen to my RRSP upon my death?

On your death, you can transfer your RRSP to your spouse’s RRSP or RRIF tax-free. The RRSP will form part of your annual net worth in case you are not married.

Q5: Can RRSP contributions be deducted annually?

RRSP contributions qualify for immediate tax relief as they are tax deductible and could be used to reduce one’s taxable income annually.